•

Plans

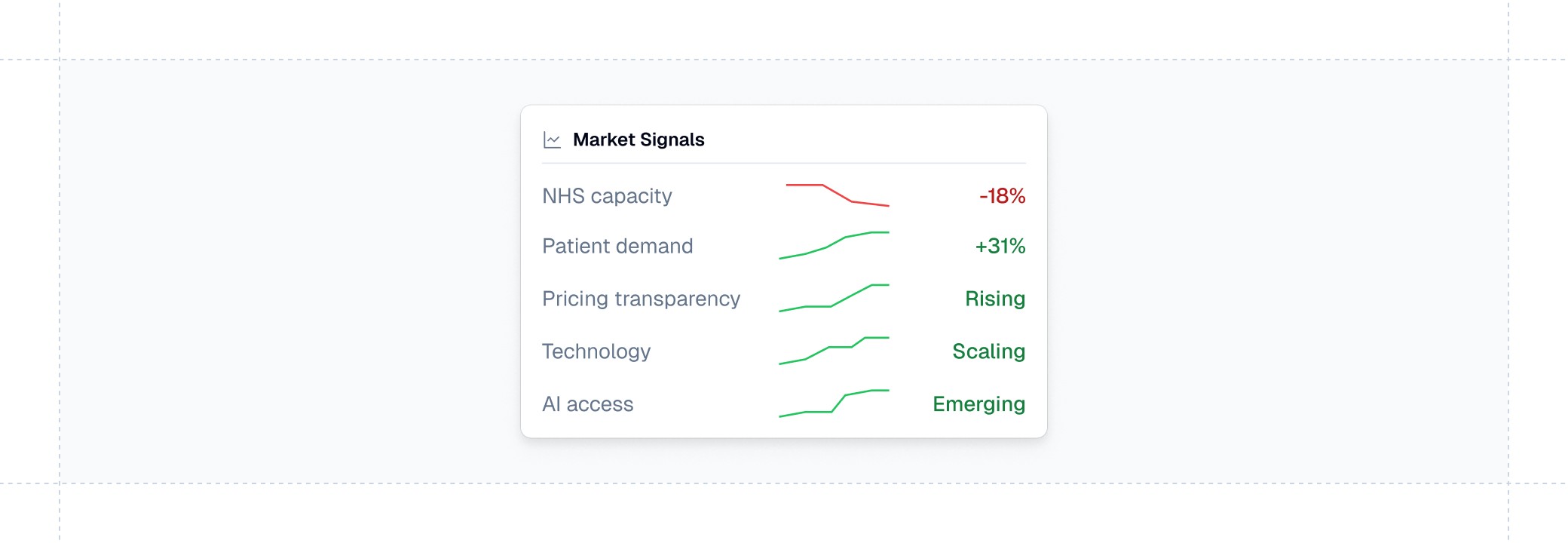

The Five Tectonic Forces Reshaping Dentistry

The transformation of dental memberships is not driven by a single innovation or isolated trend.

It is the result of five structural forces that are reshaping how dental care is accessed, delivered, and monetised.

These forces are:

long-term

mutually reinforcing

and already in motion

Together, they do not incrementally improve the existing model — they fundamentally redefine it.

1. NHS Capacity Constraint

A structural access crisis

The UK dental system is undergoing a sustained reduction in NHS capacity, driven by:

long-term underfunding

contract misalignment (UDA model)

and workforce shortages

Dentists are increasingly:

reducing NHS exposure

or exiting entirely

This creates a structural shift: access to routine dental care is no longer guaranteed for a large portion of the population. This is not cyclical — it is systemic.

2. Consumer Demand for Access

From optional care to guaranteed access

As NHS availability declines, patient behaviour changes. The key shift is not willingness to pay more.

It is: willingness to pay for certainty.

Patients increasingly prioritise:

access to appointments

continuity of care

and predictable availability

Memberships become the mechanism through which access is secured.

This reframes the value proposition:

from “discounted care”

to “guaranteed access”

3. Pricing Transparency & Economic Pressure

The unbundling of the model

Historically, dental plans have been priced as bundled products, combining:

administration

A&E or scheme components

and onboarding fees

This limited scrutiny of individual elements. That is now changing.

Practices — particularly larger groups — are increasingly:

separating pricing components

benchmarking providers

and renegotiating contracts

This exposes:

the true cost of administration

the limited value of certain components (e.g. A&E)

and significant variation across providers

The result is:

downward pressure on pricing and a structural reset of provider economics.

4. Technology Enablement

Infrastructure enables a new model

The shift to cloud-based practice management systems marks a fundamental change in infrastructure.

Modern platforms (e.g. Dentally, CareStack) enable:

real-time data access

integration across systems

and scalable digital workflows

This allows practices to move beyond:

manual processes

and fragmented systems

toward:

structured patient journeys

centralised management

and repeatable growth processes

Technology does not create demand — but it makes a new operating model possible.

5. AI & Digital Patient Access

A step-change in interaction and scale

Artificial intelligence builds on this infrastructure to transform how patients interact with practices.

Conversational interfaces (chat and voice) enable:

appointment booking

treatment inquiry

and membership sign-up

without requiring:

forms

or manual intervention

At the same time, AI enables:

proactive outbound engagement

personalised communication

and continuous optimisation of conversion

This represents a shift from:

reactive, staff-driven processes

to:

system-driven, always-on patient engagement.

How these forces interact

These forces do not operate independently.

They form a reinforcing system:

NHS constraints create the need for access

consumer demand defines the value proposition

pricing transparency reshapes the economics

technology enables execution

AI accelerates scale and efficiency

What this means for the market

At their intersection, these forces are driving a fundamental transformation:

dental plans are evolving into technology-enabled access systems

This shift affects:

pricing structures

product design

distribution channels

and competitive dynamics

It also changes the role of the practice:

from provider of episodic care

to manager of continuous patient relationships

Closing line

The following chapters examine how these forces translate into concrete changes across pricing, product design, growth, and competition — and what this means in practice.

Why this version works

Adds depth without losing clarity

Keeps the cause → effect logic clean

Aligns perfectly with:

your visual

your chapters

your executive summary