•

Plans

Market Repricing: How Dental Membership Economics Are Changing

Chapter Two

In Chapter 1 we examined how increasing pricing transparency is beginning to reshape the dental membership market. As practices gain visibility into the structure of plan pricing and compare providers more easily, long-standing assumptions about the cost of administering memberships are being challenged.

This transparency is now leading to the next stage of market evolution: repricing.

Repricing does not occur through a single adjustment. Instead, it is unfolding across several components of the traditional dental plan model:

administration fees

insurance or scheme revenue

sign-up fees for new members

legacy high-priced contracts.

Understanding how these elements interact is essential to understanding how the industry’s economics are evolving.

The true structure of dental plan pricing

One of the defining characteristics of the dental plan industry has been the bundling of multiple economic components into a single monthly fee.

Practices typically see only a headline monthly cost per member. However, that cost historically combines two distinct elements:

membership administration

accident and emergency (A&E) cover or scheme revenue

Separating these elements reveals a much clearer picture of the underlying economics.

Graph — Typical structure of plan pricing

Component | Typical value |

Administration | £0.60 – £1.40 |

A&E / scheme cover | £0.30 – £0.60 |

Total monthly fee | £1.00 – £2.00 |

The variation across providers reflects different historical approaches to structuring plan economics.

Three pricing architectures in the market

The UK dental plan market has historically operated under three distinct pricing models.

Denplan: separated administration and insurance

Denplan historically priced its plans with a clear separation between administration and insurance.

Typical structure:

Component | Approximate value |

Administration fee | ~£1.00 – £2.00 |

A&E insurance | ~£0.60 |

Total | ~£2.40 (Avg) |

This model made the administration cost highly visible to practices. It also allowed Denplan to generate additional revenue through separately priced insurance.

Practice Plan: bundled pricing with scheme structure

Practice Plan adopted a different approach by bundling the components of plan pricing.

A typical structure might appear as follows:

Component (presented) | Typical value |

Administration | £0.30 – £0.40 |

Scheme / A&E cover | £0.70 – £0.90 |

Total | £1.00 – £1.30 |

However, this breakdown largely reflects tax positioning rather than underlying operational costs.

Administration services are subject to VAT, whereas scheme revenue is often structured in a way that is not. As a result, allocating more revenue to the scheme component reduces the provider’s VAT exposure.

Patient Plan Direct: lower bundled pricing

Patient Plan Direct follows a similar bundled structure, typically at lower price points.

Typical pricing appears as:

Component (presented) | Typical value |

Administration | £0.30 – £0.40 |

Scheme / A&E cover | £0.50 – £0.70 |

Total | £0.90 – £1.10 |

As with Practice Plan, the presentation reflects a combination of competitive positioning and tax optimisation rather than the pure cost of administration.

Why pricing structures are now being questioned

As pricing transparency improves, practices increasingly separate the key questions underlying these pricing models:

What does it actually cost to administer a membership?

What value does A&E cover provide?

Why are these components bundled together?

Once those questions are asked, the economics of dental plans begin to look very different.

Practices realise that administration, insurance, and marketing costs have historically been combined into a single number that is difficult to compare across providers.

Unbundling these components naturally leads to repricing.

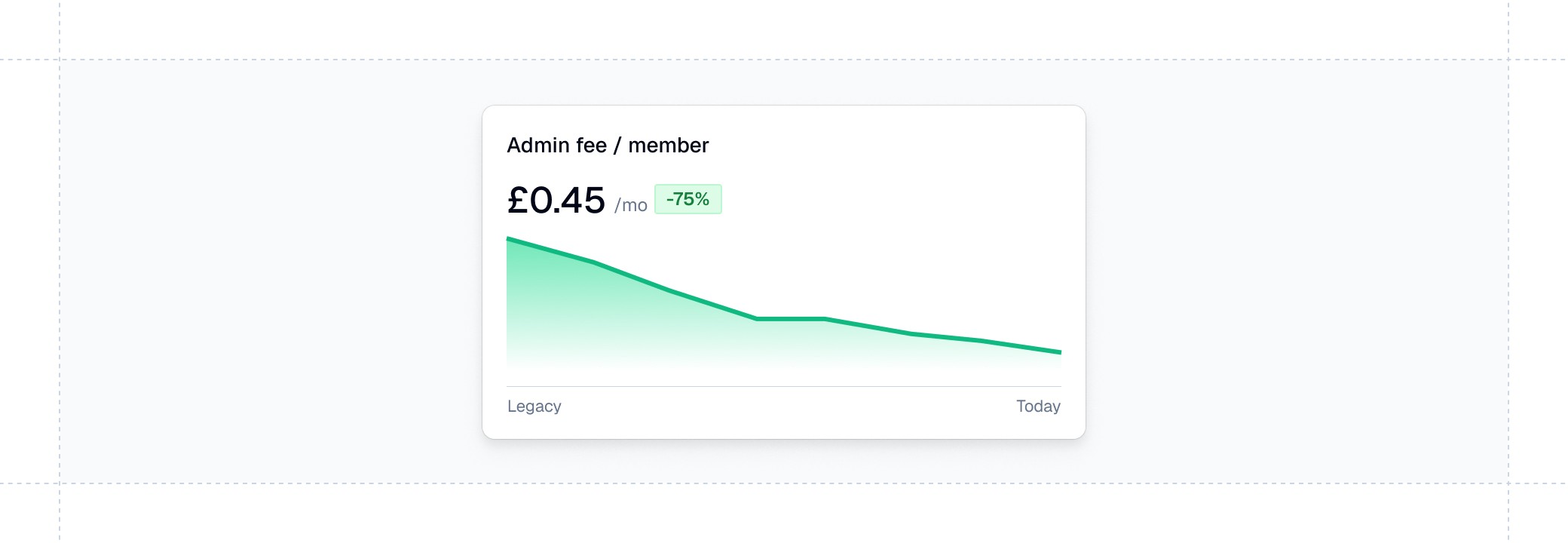

Administration fees are beginning to converge

When the insurance component is removed from plan pricing, a clearer benchmark emerges for the cost of administration.

Across larger dental groups and enterprise operators, administration fees are already converging toward:

£0.50–£0.60 per member per month (including VAT).

This represents a substantial reduction relative to historical pricing levels.

Graph — Administration fee convergence

Market segment | Historical range | Emerging benchmark |

Enterprise groups | £1.00 – £1.30 | £0.50 – £0.60 |

Mid-market practices | £0.90 – £1.20 | £0.50 – £0.70 |

Smaller practices | £1.20 – £2.00+ | ~£0.80 |

The shift reflects two structural changes:

improved pricing transparency across the market

the lower operational cost of digital membership platforms.

The role of sign-up fees

Another component of repricing concerns sign-up fees for new members.

Historically, smaller practices often paid fees ranging between:

£5 and £10 per new member

when onboarding patients into a plan.

These fees supported traditional account management activities, including:

local marketing support

practice visits from account managers

printed marketing materials

manual onboarding assistance.

In a digital membership environment, many of these activities become automated.

Online sign-up journeys, QR codes, automated direct debit authorisation, and integrated practice systems dramatically reduce the cost of onboarding new members.

As a result, sign-up fees are gradually disappearing from the market.

Graph — Evolution of plan economics

Revenue component | Traditional model | Emerging model |

Administration | £1.00 – £1.50 | £0.50 – £0.80 |

A&E / scheme | £0.30 – £0.60 | optional add-on |

Sign-up fees | £5 – £10 per member | largely eliminated |

Together, these changes illustrate how repricing affects multiple revenue streams simultaneously.

Implications for the industry

The repricing of administration fees, insurance margins, and sign-up economics has significant implications for the dental plan industry.

Historically, plan providers generated revenue from a combination of:

administration fees

insurance products

scheme revenue structures

onboarding fees.

As these components become more transparent and increasingly separated, the revenue model of the industry is evolving.

At the same time, however, demand for dental memberships continues to grow as access to NHS dentistry declines and practices expand private care.

This creates a paradox:

Revenue per member may fall, while the total number of members increases.

The overall size of the membership market may therefore continue to expand even as individual pricing components decline.

The next question for the industry

If administration costs are falling and sign-up fees are disappearing, one element of the traditional plan structure becomes increasingly visible:

accident and emergency cover.

Many membership plans continue to bundle A&E cover as a core component of their pricing.

However, as practices and patients look more closely at the value of these schemes, an important question emerges:

How often is this cover actually used?

The next chapter explores the economics of accident and emergency cover and its role in the future structure of dental memberships.